What’s driving FinTech innovation?

When it comes to financial services, the world saw a shifting in customer needs worldwide that outpaced global banking systems’ ability to adapt to these demands. This acted as a fertile field for the rise of FinTech.

Since, new customer-centric entrants have emerged outside of the traditional banking system, determined to improve the user experience, transparency, and value-for-money. These players were able to innovate at a rapid pace by mainly focusing on single product offerings. However, as the FinTech industry matures, we are witnessing a new wave of innovation, led by two mega trends:

- Financial services and insurance are offering products and services that are tailored to the demands of their target market. This allows single-product companies to create even more targeted offerings, enabling them to improve their share of wallet and diversify their income sources.

- Fundamental banking infrastructure and supporting technologies are enabling non-financial enterprises to introduce financial products to complement their current offers. This also allows established financial service providers to redesign their back-ends.

As a sector, FinTech is an investor magnet

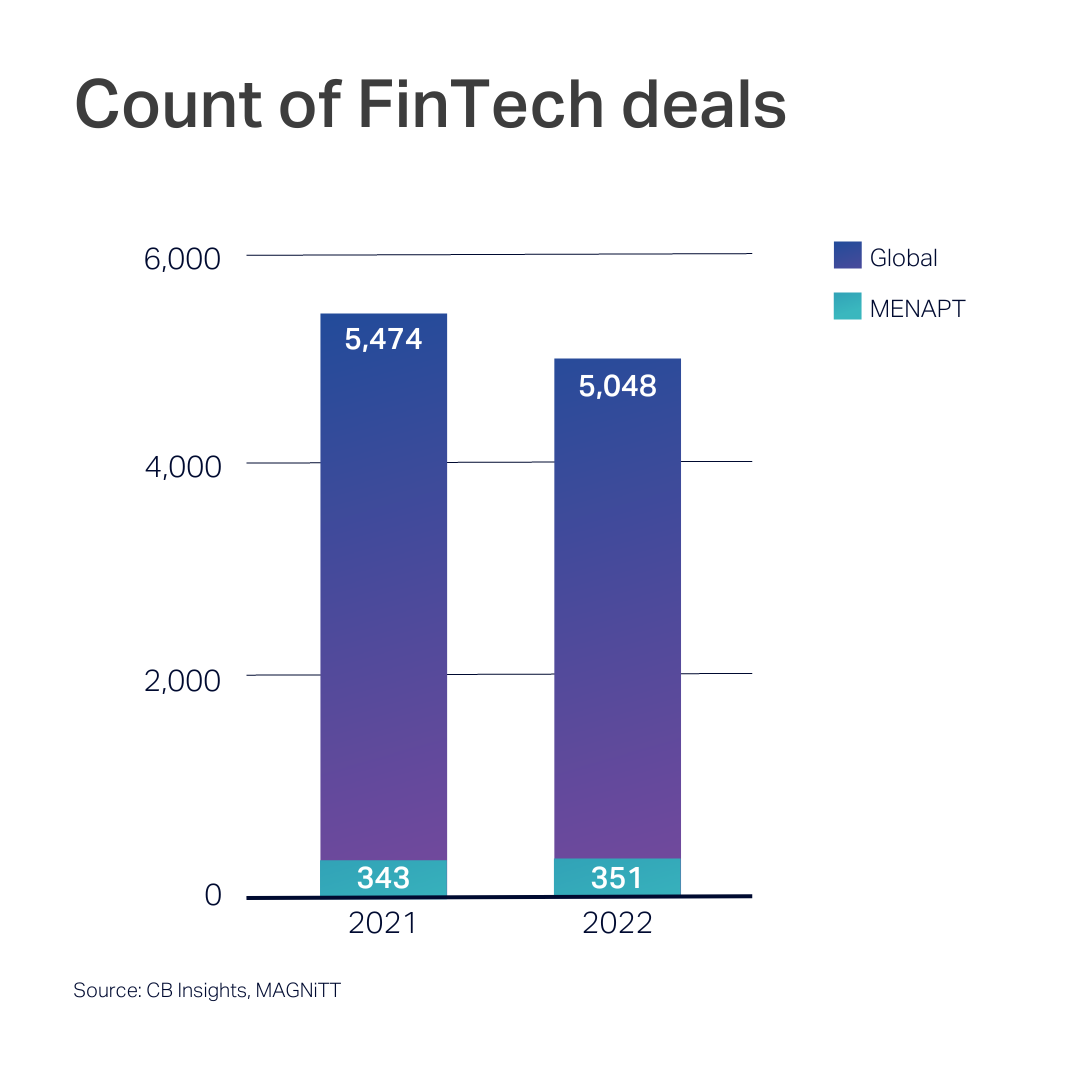

FinTechs have received over $350 billion in venture capital funding globally over the last 5 years across nearly 21,000 deals (according to CB Insights), covering the whole financial services industry, from money transfers to banking, lending to payments, and insurance to financial business tools. As a result, several FinTechs Unicorns have been created.

According to CB Insights, though investments in the sector dropped in 2021 compared to the year-before, the amount invested that year exceeding all prior years’ funding volume. Therefore, venture activity in the sector has seen an overall upwards trends globally, when you factor out the global slowdown in startup activity and valuations in 2021 (which we’ve previously written about here). In fact, FinTech was the most invested sector of tech in 2022, making it the most attractive sector for investors — implying a strong premise for future opportunity.

When looking at FinTech investment activity in the MENAPT region, it’s the most invested-in sector in venture capital, by both deal volume and count, at $2,256 million invested across 351 deals (according to MAGNiTT). When zooming in on the Middle East, the UAE saw the most VC activity in the FinTech sector in 2022, also across both deal volume and count.

The need for innovation across the financial industry

Wherever they may be located, people need access to financial services in order to grow their enterprises and prepare for life’s ups and downs. Up until recently, obtaining these services typically required onerous red tape and expensive expenses, not to mention leaving entire populations of people behind to be unbanked.

As a result, this age of digitization and decentralized technology makes it possible to readily offer communities around the world banking services in ways that weren’t previously possible. They may accomplish this while providing a noticeably better service at a lower cost of execution (when compared to conventional financial providers), or in many circumstances, where there are no established competitors.

As Andreessen Horowitz often stated, every business will eventually turn into a FinTech company. The world is only beginning. We at DFDF will be ready to seize this upcoming new wave, building up on the experience we are constructing while investing in the UAE.

Our Future of Finance thesis

FinTech is largely viewed narrowly to include banking services, payments, lending, and insurance. However, there are numerous structural factors driving FinTech ahead, including the advent of Stripe, Plaid, and other infrastructure-defining decacorns that enabled business models and applications that were not really thinkable a few years ago — think only to the general API-ification of the typical tech stack.

We believe that holding FinTech as a fresh business model for online businesses is a more comprehensive perspective. We also believe that the global opportunity is significantly greater in that environment. For example, considering the characteristics of the GCC region, cross-border and worldwide enablers are, therefore, a major focus, and wealth management is something we will be putting a lot of attention into.

However, this topic now has entirely new implications from what it did in the past. It entails fresh clientele that can be reached as well as asset classes like cryptocurrency that you could not have previously associated with wealth management.

Our view on Future of Finance verticals

In light of this, we have outlined a handful of crucial applications that FinTechs are currently tackling. All around the world, we are witnessing the emergence of numerous innovative and alternative business models, and we are dedicated to funding those that will revolutionize the way that businesses access and offer financial services.

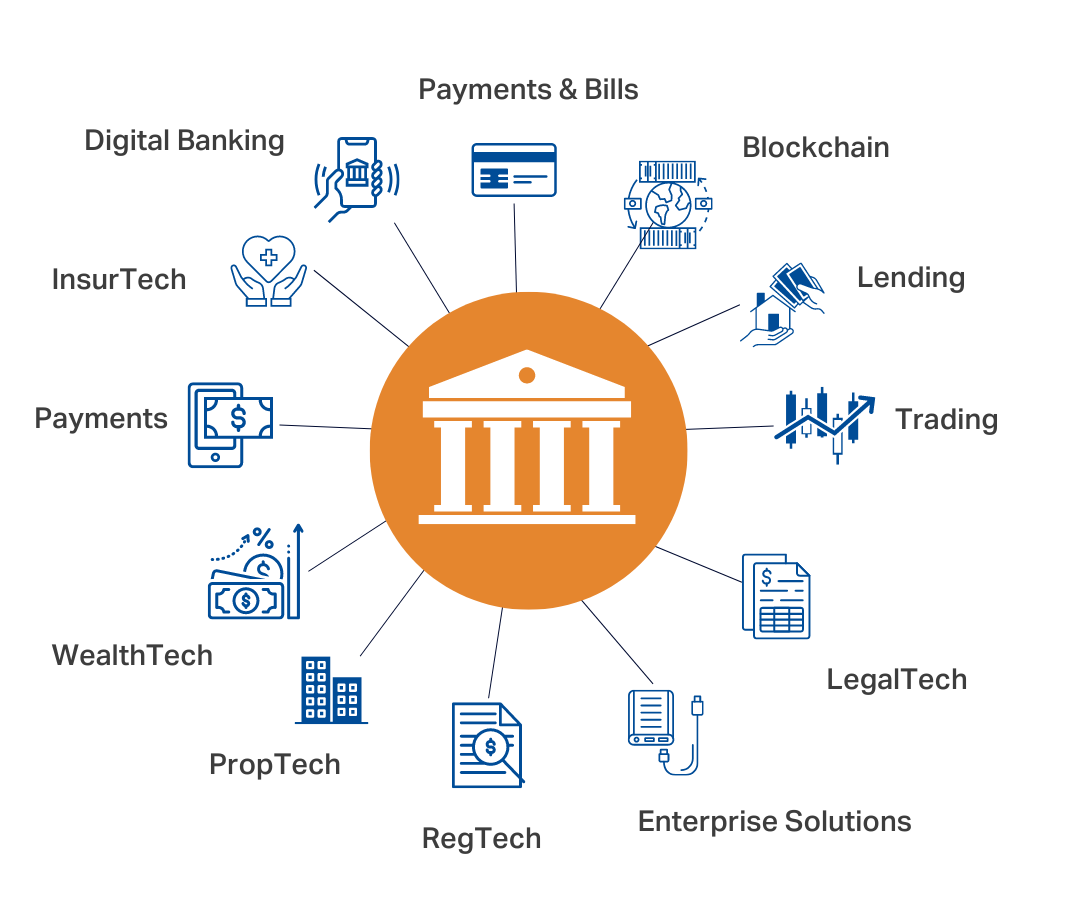

Specifically, when looking at the broad FinTech landscape, DFDF aims at covering the following verticals:

A. Digital banking

B. Bill management and payments

C. InsurTech

D. Lending

E. Remittances

F. Trading & Capital Markets

G. Wealth Management

H. Mortgage and Real Estate

I. Blockchain and its B2B applications

J. RegTech / LegalTech

K. Enterprise Solutions and Infrastructure

Within these verticals, we distinguish between the three macro categories of vertical application, namely:

1. Front End Applications: Final products and solutions used by businesses to manage the finances or the transactions.

2. Mid Tier: Final products and solutions used by business to eliminate the need for integration with legacy tech infrastructure and subsequent front-end applications.

3. Infrastructure: Underlying products and solutions used by businesses to provide their core services to other businesses, e.g. BaaS (banking as a service), security, AML and KYC.

The FinTech business models in our thesis

We describe FinTech as those products that are customer-focused, mobile-first, and disruptive to risk-averse sectors. However, the industry’s scope is far wider, encompassing the accounting departments and financial records of banks, insurance companies, property management companies, governmental agencies, and more — payments, insurance underwriting, claims processing, lending disbursement, RegTech, risk management, accounting are all examples of financial services that may be supported by FinTech companies. Broadly speaking, all the actors who are integrating technology into financial services are FinTech businesses. They are demonstrating how to use technology to raise the bar for finance.

Future developments in FinTech will be characterized by data and access, with ubiquitous mobility enabling fast access to the customer and instant access to consumer data. Concerns about environmental, social, and governance regulations are also becoming more and more important in the context of FinTech, especially as millennials and Generation Z take the head of businesses. Moreover, in order to tackle the industry’s more challenging issues, such as cybersecurity, specifically anti-cyber-fraud, and egTech, the FinTech movement is moving somewhat away from customer-facing apps as it matures – aiming to digitize and streamline the strict regulatory landscape that financial services companies must face.

Now that we have defined the industry and have laid down the cornerstones of our investment manifesto, the following is a deep-dive on what we have witnessed so far as the most compelling models in MENAPT FinTech, where we have also allocated some resources already.

FinTech technology and infrastructure enablers

APIs generally — and more specifically, financial infrastructure APIs — have attracted a lot of interest as a result of the growth of open banking over the past three to four years. According to Research and Markets, the open banking market will expand at a compound annual growth rate of 24.4% from 2019 to 2026. However, if FinTech companies and banks can gain the confidence and business from a growing global client base, the market might expand much more quickly. In particular, APIs have spared FinTech companies, and even larger corporations, the headache of having to construct complete stacks from scratch. Smaller businesses can compete with larger organizations by using APIs to address problems that were overlooked or postponed because to inability.

Amongst API infrastructure players, we identify BaaS as a segment particularly worthy of close attention. A BaaS product is one that combines all of the components a business may require to launch financial services and makes them accessible via API. These BaaS providers typically charge a platform fee to clients and/or split the profits from interchange or other fees brought in by the client’s final good or service. Hooking into an API or group of APIs can be a low-cost, hassle-free approach to create, test, and deploy for FinTech startups or vertical SaaS firms looking to deliver financial services without assembling a brand-new fintech workforce.

BaaS businesses have raised money this year, including NY-based Unit, which raised $51 million in a Series B round in June to advance its objective of enabling businesses and FinTechs to create banking solutions “in minutes.” Additionally, a Berlin startup called Solarisbank raised $224 million at a $1.65 billion value in July. Solarisbank offers a variety of financial services via 180 APIs that other companies may use to create end-user-facing solutions. In the UAE, we’ve identified Nymcard as our pick in the Banking-as-a-Service (BaaS) category.

Founded in 2018 by Omar Onsi, NymCard is a MENA-based BaaS provider of embedded finance infrastructure. It offers a cloud-based modern payment issuing and processing platform allowing FinTechs, large enterprises, and banks with legacy platforms in the MENA region to instantly create, control, and distribute virtual or physical payment cards. NymCard works in a flexible and locally relevant approach in each country by partnering with local financial institutions and providing operational support for running the service locally while leveraging a common product for agility and economies of scale. Through strategic partnerships, they offer clients fast tracking card issuance in 6 countries – UAE, Jordan, Iraq, Bahrain, Malaysia, and the Philippines. With NymCard, FinTechs can integrate with the payments ecosystem through a simple plug and play framework, without worrying about back-end complexities.

The future of consumer finance is more personalized

In our opinion, consumer FinTech will essentially resemble traditional banking, with broad, large-scale platforms but with services for fundamental consumer needs and focused, vertical services for niche markets with particular requirements and value propositions. Additionally, vertically-focused FinTechs are now able to gather segmented audiences across geographies in ways that were previously impossible thanks to the internet.

The development of traditional banking contributes to the explanation of why consumer FinTech firms that initially seem competitive are actually offering distinct services. Consumer FinTechs serve diverse customers with various value propositions, similar to how community banks and credit unions have prospered by concentrating on small vertical audiences. However, consumer FinTechs may utilize the internet to more readily aggregate a customer segment — for example, Islamic finance or Gen Z students — and the UAE is witnessing this trend as well.

While products may initially find a niche by innovating on one primitive (savings, spending, lending, or investing), what will distinguish these products in the long-run will be the features that are specifically designed for a particular community or audience. As consumer FinTech continues to grow, we expect to see the rise of many winners.

We’ve identified Zywa as the startup that is at the forefront of this trend in the UAE. Founded in 2020 by Alok Kumar and Nuha Hashem, Zywa is a FinTech company offering a neobank for kids. We got to know Zywa through its affiliate DIFC FinTech Hive. Through Zywa, teens are able to spend, receive and manage money without the need for cash. They can also earn rewards and interact with their friends on the platform. Using the app, parents can send money to their kids, which they can spend securely in the safe environment of their parents’ oversight. Serving a $13B market opportunity in the MENA region, Zywa was admitted to Y Combinator (YC) in their Winter 2022 batch and aims to be the payments and financial platform of choice for older teenagers, focused on personality and customization, and is the first to launch in the region.

Processing employee benefits will be streamlined

While money is unquestionably the primary attraction in a company’s compensation package, additional “perks” can help sweeten the deal for current or potential employees. These could range from pension schemes to gym subsidies or support for mental health. We see a rising demand for technology that requires talent to be hired and retained, though the world is currently going through a “great resignation” where attracting this talent is challenging. Players in this space include Peakon, which was acquired by Workday for $700 million last year, JobandTalent, which reached a valuation of $2.35 in December, and Gympass, which most recently reached a valuation of $2.2 billion.

When looking at the employee benefits world in the UAE, we’ve identified FinFlx as one of the startups ready to seize the opportunity in employee benefits. Founded in 2019 by Amr Yussif and Matthieu Capelle, FinFlx is a cloud-based B2B2C employee financial wellbeing platform that was part of Y Combinator batch of Winter 2022 and FinTech Hive affiliated. The company’s core product offering is a portable 401k plan, supplemented by a financial literacy and micro-lending platform, built to integrate seamlessly with other tech providers (e.g. brokers, custodian, payroll, accounting and reporting). Serving a $12 billion gratuity contribution market in the UAE alone, FinFlx aims to be the pension-provider and investment platform of choice charging only 50bps on invested capital.

The intersection of finance and real estate will be disrupted

We are all aware that the housing market has cycles. More purchases and refinances result from low interest rates. Due to historically low interest rates in 2020, both rates and purchases increased. Aspiring home buyers took advantage of the cheap rates to buy homes, while existing home purchasers rushed to change the terms of their loans. Home took on a new meaning when you consider that more individuals were spending more time at home than ever before as a result of COVID shelter-in-place orders. Many people now require extra space. Others relocated to new residences by taking advantage of new remote work regulations and being hampered by commutes.

In this current environment of liquidity tightening coupled with a scarcity in housing supply, we’re particularly attentive to startups that can facilitate and enable seamless transactions and refinances while ensuring purchasers’ peace of mind, especially in the thriving market for real estate of Dubai. Therefore, we are looking for solutions able to support the growth and the liquidity of the market in the region.

Founded in 2020 by Arran Summerhill and Michael Hunter, Holo is a Dubai-based PropTech brokerage company that is digitizing the traditional mortgage and subsequently home-buying process. The company seeks to simplify the home buying process and capture the $57 billion under-penetrated property market in the UAE. It has built a platform that connects all stages of the mortgage buying process onto one centralized platform, allowing buyers to track, monitor and manage the process digitally. Holo enables customers to secure home loans through its web and mobile app, without any paperwork. The platform essentially finds the mortgage plans that match users’ needs, obtain pre-approvals from the banks and help to close the deals.

Finance will be decentralized at large

Decentralized Finance (a.k.a. “DeFi”) is made up of a growing number of systems that support financial applications for lending, trading, and other activities. Even though only a small portion of financial services transactions are currently conducted using cryptocurrencies (coins or tokens) as opposed to those conducted using fiat (government-issued) currencies like the U.S. Dollar, that number is rapidly increasing. Just between January 2021 and December 2021, these transactions increased by 400%, according to CB Insights. Notwithstanding the “crypto winter” (that we talked about in a previous blog post here), 2022 was still say investments in the space — particularly at the early stage level. In fact, DeFi-specialized VC Polychain Capital remained the most active Fintech investor by amount of deals in 2022 (according to CB insights).

We believe that DeFi has enormous potential to penetrate traditional finance as well as crypto trading, especially in:

1. Lending and borrowing: DeFi services connect lenders and borrowers, uphold loan terms, and disburse interest automatically. Yield farming, or leasing cryptocurrency assets in return for transaction costs or interest, has recently become a well-liked method for generating passive income.

2. Decentralized insurance: In the crypto ecosystem, users can buy insurance to cover losses of digital assets. Without utilizing a traditional insurance broker or agent, a DeFi platform connects customers looking for coverage with those ready to insure them in exchange for payment of premiums.

3. Decentralized exchanges: Users can purchase, sell, or trade cryptocurrencies on decentralized exchanges (DEXs). There is no exchange operator, no need to verify your identity, and no withdrawal fees when users trade on a DEX. Instead, through automated market-maker protocols, the smart contracts enforce the rules, carry out deals, and securely handle cash. Derivative exchanges (DEXs) sometimes do not demand money be deposited into an exchange account prior to performing a trade, eliminating the main risk.

Moreover, when taking a broader MENA perspective, many unbanked or underbanked people have the option to engage in the global financial system on an inexpensive basis because to DeFi’s decentralized and open-platform design. For a large portion of the population, the traditional financial system made it impossible to interact at a low cost (through payments or remittances), invest in or hedge market or currency risks (by purchasing stocks or holding stablecoins versus local unstable currencies), or be inclusive. There is a chance for nations to advance beyond traditional technologies and take the lead, as has happened in markets like MENA, given the unique advantages that DeFi has in Emerging Markets versus established markets. As a consequence, we are particularly attentive to the applications of DeFi for FinTech that are arising in the MENA region.

If you are a founder who’s building a FinTech venture, please reach out to us, we’d love to hear from you.